The Bureau of Internal Revenue (BIR) released Revenue Memorandum Circular (RMC) No. 116-2019 with subject, “Clarifications on the Treatment of Alien Individuals Employed in the Philippines by Regional or Area Headquarters and Regional Operating Headquarters of Multinational Companies, Offshore Banking Units and Petroleum Service Contractors and Subcontractors Pursuant to Section 4.C of Revenue Regulations No. 8-2018”.

Clarifications by the BIR

RMC No. 116-2019 clarified as follows:

- For those alien individuals employed by regional or area headquarters and regional operating headquarters or multinational companies, offshore banking units and petroleum service contractor and subcontractor, they are similarly taxed as income of regular employees of locally established entities.

Thus, these alien individuals are subject to the same administrative requirement of the BIR being imposed to regular employees, such as substituted filing, issuance of BIR Form No. 2316, inclusion in the monthly withholding tax remittance on compensation, as well as in the prescribed alphalists, etc.

- For those “seconded employees or secondees”, they are likewise subject to the regular income tax rates. Thus, seconded employees shall comply the same administrative requirements except for substituted filing. In addition, the following procedures apply:

“(a) A separate employment status and description for ‘seconded employees” shall be provided in the “Current Employment Status” of the Alphabetical List of Employees/Payees from Whom Taxes Were Withheld under BIR Form No. 1604C, as well as in the Alphalist Data Entry and Validation Module version 6.1.

(b) These “seconded employees” shall file their annual income tax return and pay the income tax due, if applicable, on or before the prescribe deadline of April 15 of each year, together with the attached BIR Form No. 2316 issued by the local entities.

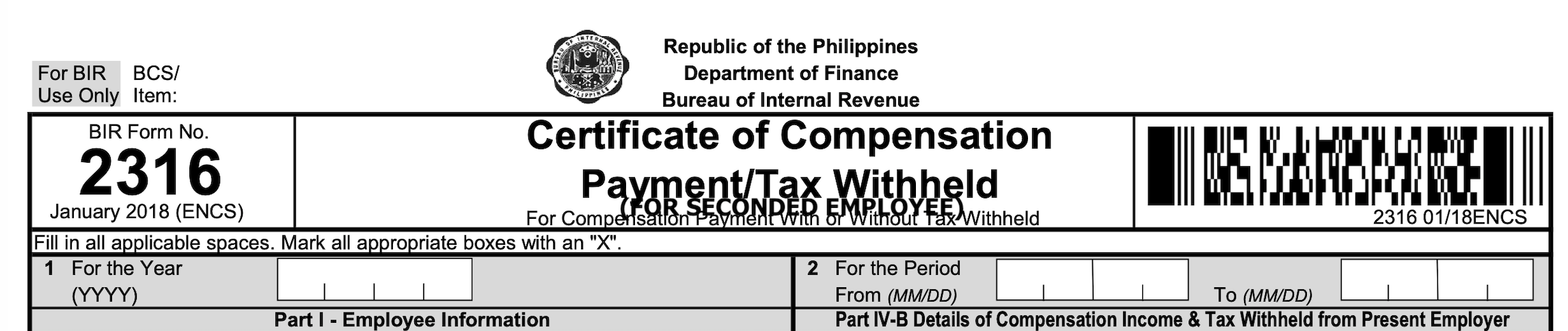

(c) In all copies of BIR Form No. 2316 to be issued to these employees, the phrase “For Seconded Employee” shall be typed or printed in bold, capital letters enclosed in open and close parenthesis immediately under the form’s title “Certificate of Compensation Payment/Tax Withheld”.

(d) In case of termination of their services before the end of the taxable year, the local entities shall ensure that the withholding tax on their last salaries shall be computed using the annualized withholding tax method, pursuant to the provisions of Sec. 2.29.(B).(5).b) of RR No. 2-98, as amended.”

Seconded employees are those alien individuals who are employed by foreign principals and who are assigned to render services exclusively to these local entities.